Paying off multiple debts can feel like trying to empty a bathtub with a spoon. The good news is that both the debt snowball and debt avalanche methods simplify the job: make the minimum payment on every debt, then put all extra money toward one target balance at a time.

The main difference is simple. Snowball goes after the smallest balance first. Avalanche attacks the highest interest rate first. That choice matters, especially when the average US credit card APR is 23.72% in March 2026, and credit card balances remain near record highs.

Here’s how each method works, where each one helps most, and how to choose the one you’ll stick with.

How the debt snowball method works, step by step

The debt snowball method focuses on balance size, not interest rate. You list every debt from the smallest balance to the largest. Then you keep paying the minimum on all of them, while sending every extra dollar to the smallest one.

The process looks like this:

- List all debts from smallest balance to largest.

- Pay the minimum due on every account.

- Put extra money toward the smallest balance.

- Once that debt is gone, roll its payment into the next smallest debt.

That last part is where the “snowball” idea comes from. Each paid-off balance frees up more cash for the next one. So your payment power grows over time, like a snowball rolling downhill.

For example, say you owe $400 on a store card, $1,800 on a credit card, and $9,000 on a car loan. With snowball, you’d attack the $400 first, even if the credit card rate is much higher. That can feel odd at first. Still, the method is built around momentum, not pure math.

Why paying off the smallest balance first feels motivating

Small wins matter because debt is emotional, not only financial. When you wipe out one account quickly, you get proof that your plan is working. That early progress can lower stress and help you keep going.

Many people quit debt plans because the finish line feels too far away. Snowball shortens that mental distance. Even one paid-off balance can turn “I’m drowning” into “I can do this.”

That’s why the method has such a loyal following. Ramsey’s explanation of the debt snowball leans heavily on this idea: behavior changes faster when you see results early.

Where the snowball method can cost you more over time

The downside is straightforward. Snowball ignores interest rates at the start. So while you’re paying off a small low-rate debt, a larger high-rate balance may keep piling up interest.

That can raise your total cost before you become debt-free. In other words, snowball often gives you a faster first win, but it may cost more overall.

For some people, that trade-off is worth it. If motivation has been the missing piece, snowball can be the method that finally sticks.

How the debt avalanche method works, step by step

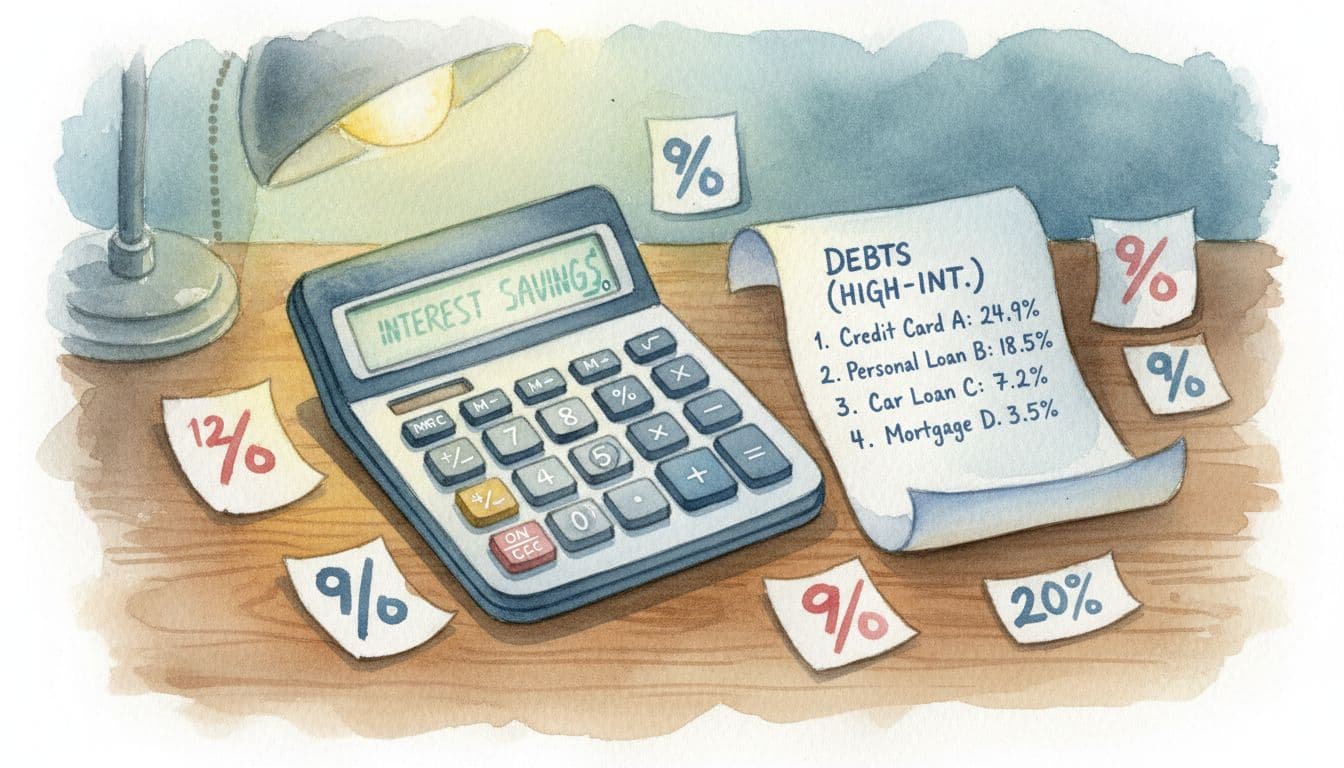

The debt avalanche method uses a different rule. Instead of sorting debts by balance, you sort them by interest rate, from highest to lowest. Then you pay minimums on everything and throw extra money at the debt charging the most interest.

The steps are simple:

- List all debts from highest APR to lowest APR.

- Pay the minimum on every account.

- Put extra money toward the highest-rate debt first.

- After that debt is gone, move to the next highest rate.

This method is built to save the most money over time. High-interest debt grows faster, so paying it down first usually trims the total interest you’ll pay.

Think about a credit card at 29% APR versus a car loan at 6%. Even if the car loan balance is smaller, the credit card is more expensive to carry. Avalanche says to stop that leak first.

Why the avalanche method usually saves more money

This is the math-first option. Since you target the most expensive debt first, less interest builds up while you work through your balances. That usually means a lower total payoff cost, and sometimes a faster overall timeline too.

That matters even more now because credit card rates remain high. A balance sitting at 20% to 30% APR can drain your budget month after month. Discover’s comparison of snowball and avalanche explains this trade-off well: avalanche favors efficiency, while snowball favors momentum.

If saving money is your top goal, avalanche often wins on paper.

Why this method can be harder to stick with at first

The hard part is psychological. Your highest-rate debt may also be one of your biggest balances. That means you could spend months paying extra without fully knocking out an account.

As a result, progress can feel slow, even when the plan is working. You’re saving money, but you may not see a satisfying “paid in full” moment right away.

That delay can wear people down. If you’ve struggled with consistency before, avalanche can feel like dieting without ever seeing the scale move.

Snowball vs avalanche, the biggest differences that matter

At a glance, these two methods are almost twins. You still pay minimums on every account. You still focus extra money on one debt at a time. The split comes down to motivation versus math.

Here’s the plain-English difference:

- Snowball: smallest balance first, quicker emotional wins

- Avalanche: highest interest first, lower total interest cost

- Snowball: often easier to stick with early on

- Avalanche: often more efficient over the full payoff period

- Both: work best when you stay consistent every month

The fastest win versus the lowest total cost

If you want the fastest first victory, snowball usually wins. You clear a smaller balance sooner, which frees up cash flow and builds confidence.

If you want the lowest total cost, avalanche usually wins. That’s because interest keeps working against you until the highest-rate debt is gone. Money’s look at which works faster highlights the same tension: the best “fast” method depends on whether you mean fast emotional progress or fast savings on interest.

Why the best method is the one you will actually follow

A perfect plan that lasts two weeks is not perfect. Debt payoff is a long trip, and consistency matters more than bragging rights.

If a method looks better on paper but makes you quit, it’s the wrong method for you.

That’s why many personal finance writers keep coming back to behavior. Math matters. So do habits. If you’ll stay engaged with snowball, that may beat an avalanche plan you abandon after month one.

How to choose the right debt payoff method for your situation

Your best choice depends on your debt mix, your stress level, and your track record. Someone with five small balances may need quick wins. Someone with large credit card debt at high rates may care more about cutting interest.

As of the end of 2025, total US household debt reached $18.8 trillion, with credit card debt at a record $1.28 trillion. Those numbers show how common this problem is. You’re not behind because you need a system. You’re being smart by picking one.

Credit cards often make avalanche look attractive because their APRs are so high. Still, motivation can outweigh math if the math-only plan leaves you stuck.

Choose snowball if you need quick progress to stay motivated

Snowball often fits people who feel overwhelmed by too many balances. It also helps people who’ve tried to pay off debt before and lost steam.

For example, if you have several small medical bills, a store card, and a personal loan, clearing the smaller debts first can create visible progress fast. That can reduce stress and make your budget feel lighter.

Snowball is also useful if your problem hasn’t been knowledge. It’s been follow-through.

Choose avalanche if cutting interest is your top goal

Avalanche often fits people who can stay steady without early wins. If you like numbers, watch your budget closely, and want the most cost-effective path, this method may suit you better.

It can be a strong choice if most of your debt sits on high-rate credit cards. In that case, each extra payment toward the top APR can save meaningful money over time. Business Insider’s comparison of both methods makes that case clearly.

Some people even blend the two. They start with one small balance for momentum, then switch to avalanche. That can work, as long as you stay focused on one target debt at a time.

The difference between snowball and avalanche is simple: snowball pays the smallest balance first, while avalanche pays the highest interest rate first. Both can work, but neither works unless you keep paying the minimum on every debt and send every extra dollar to one target balance.

Pick the plan that feels doable tonight, not the one that sounds best in theory.

Make your debt list, choose your method, and put your next extra dollar to work.