Budgeting often feels harder than it should. You get paid, bills hit, life happens, and somehow the month ends faster than your money.

That’s why the 50/30/20 rule sticks around. It gives you a simple starting point: use your after-tax, take-home pay, not your gross salary, and split it into three buckets for needs, wants, and savings. The idea was popularized by Elizabeth Warren and Amelia Warren Tyagi in All Your Worth, and you can still find a preview of All Your Worth online.

If you want a budget that feels more like a map than a math test, this method is a solid place to begin.

How the 50/30/20 budget works, step by step

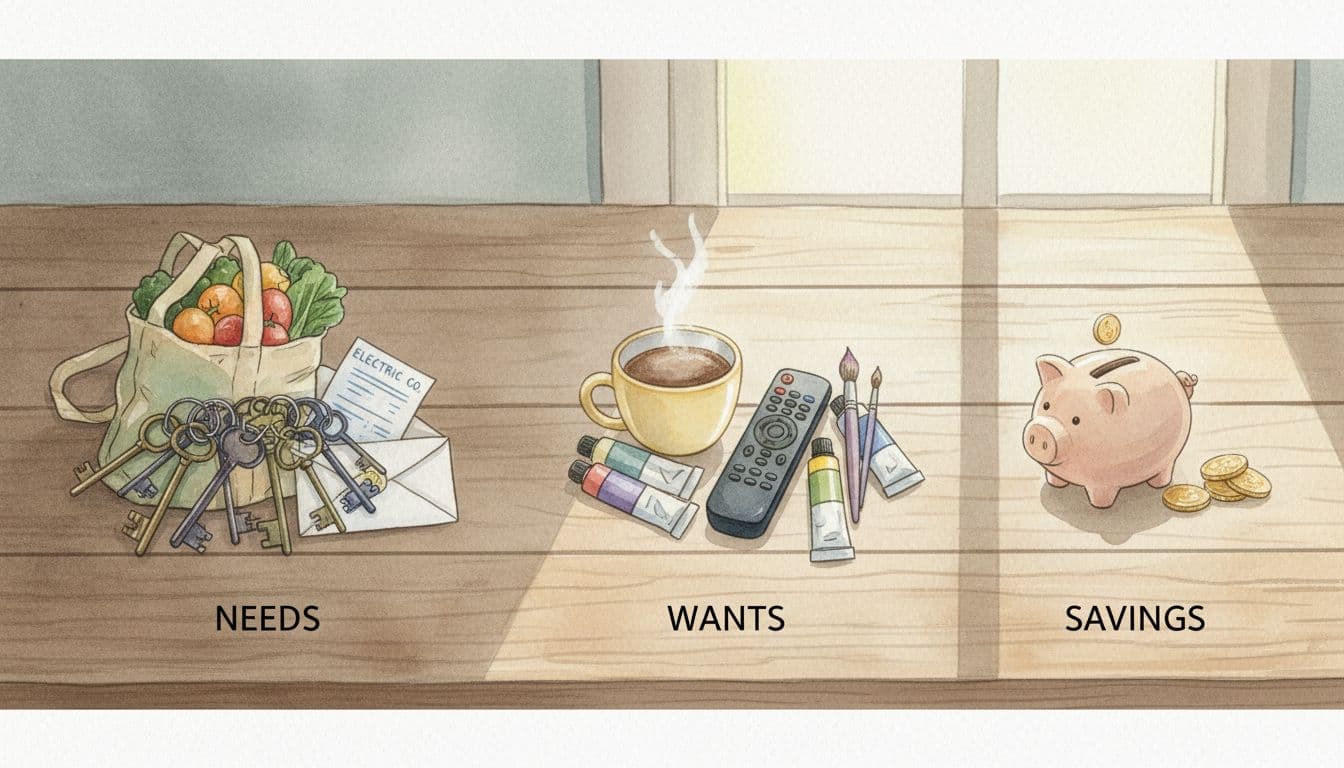

The rule is simple on paper. You take 100% of your monthly take-home pay and divide it like this:

- 50% for needs

- 30% for wants

- 20% for savings or extra debt payoff

That’s it. The percentages should add up to 100% of what lands in your bank account each month.

Start with your take-home pay, not your full salary

This is where many people go wrong. They build their budget from gross income, then wonder why the numbers never work.

Take-home pay is what you keep after taxes and payroll deductions. Depending on your paycheck, that may also mean money left after health insurance, retirement contributions, or other automatic deductions. In other words, it’s the amount you can actually spend, save, or send to debt.

Say your salary is $60,000 a year. That doesn’t mean you can divide $5,000 a month into neat buckets. Your real budget has to start with the amount that hits your checking account.

Using gross income makes the budget look bigger than real life. It’s like planning a road trip with a fuel tank that isn’t full. The map may look fine, but the car won’t make it.

What counts as needs, wants, and savings or debt payoff

The three buckets sound easy, but the details matter.

Needs are the bills you must cover to live and work. That can include housing, groceries, utilities, transportation, insurance, health care, child care, and minimum debt payments. If skipping it would cause a serious problem, it usually belongs here.

Wants are the extras that make life more fun or comfortable. Think dining out, streaming services, hobbies, shopping, concert tickets, travel, and entertainment. These aren’t “bad” expenses. They’re simply optional.

Savings or debt payoff covers your future goals. This bucket can include your emergency fund, retirement contributions outside payroll, sinking funds for car repairs or holidays, a down payment fund, and extra payments on debt. Here’s the key line: minimum debt payments go in needs, but extra debt payments go in the 20% bucket.

That split keeps the method honest. A plain-English overview of the rule makes the same point, and it’s one reason the system stays easy to use.

A simple 50/30/20 example you can copy

The math gets much easier once you see the rule in action. Let’s use clean numbers.

Example budget for a $3,000 monthly take-home income

If your take-home pay is $3,000 a month, the split looks like this:

| Bucket | Target Amount | Example line items |

|---|---|---|

| Needs | $1,500 | Rent $950, groceries $250, utilities $100, gas/transit $100, insurance/copays $50, minimum debt payment $50 |

| Wants | $900 | Dining out $250, streaming/gym $80, hobbies $120, shopping $200, fun money $250 |

| Savings or extra debt payoff | $600 | Emergency fund $250, Roth IRA $200, extra student loan payment $150 |

The point isn’t to copy those exact line items. The point is to see how the three buckets guide your choices. If your needs total $1,700, then you already know something has to give. Either costs need to drop, income needs to rise, or your percentages need a short-term adjustment.

A lot of people like this method because it answers one basic question fast: “How much room do I actually have?” If you want more ideas, these real-life 50/30/20 budget examples can help you picture your own numbers.

How the rule can look at lower and higher income levels

The math stays the same across income levels. Still, the pressure inside each bucket can feel wildly different.

At $2,000 a month, your targets are $1,000 for needs, $600 for wants, and $400 for savings or extra debt payoff. That may feel tight, especially if rent takes half your income.

At $5,000 a month, the split becomes $2,500, $1,500, and $1,000. There’s often more breathing room, so the rule may feel easier to follow.

At $10,000 a month, the targets rise to $5,000, $3,000, and $2,000. The percentages still work, but lifestyle creep can sneak in. Bigger income doesn’t always mean better habits.

Location matters too. In many high-cost US cities, housing alone can eat 35% to 45% of take-home pay in 2026. When that happens, keeping all needs under 50% may not be realistic.

Why people like this budgeting rule, and where it can fall short

No budget method works for every person in every season. The 50/30/20 rule earns praise for good reason, but it also has limits.

The biggest benefits of the 50/30/20 rule

Its biggest strength is simplicity. You don’t need a spreadsheet with 40 categories. You don’t need to track every coffee on day one. You only need to know where your spending fits.

It’s also flexible. Within the wants bucket, you can choose what matters most to you. Maybe you care more about travel than takeout. Maybe you’d rather spend less on shopping and more on live events. The rule leaves room for real life.

Another benefit is balance. Some budgets focus so hard on cutting that they feel punishing. Others ignore savings until “later.” This rule gives space to enjoy today while still paying attention to tomorrow. That balance helps many beginners stick with it.

There’s a reason it still gets heavy attention in 2026, especially across social media finance communities. The idea is easy to explain, easy to remember, and easy to try. A broader look at Citi’s 50/30/20 explainer shows why it remains a popular starting framework.

When the 50/30/20 rule may not fit your situation

The weak spot is also obvious: real life doesn’t always fit neat percentages.

If you live in an expensive city, support a large family, have high child care costs, or carry heavy debt, your needs may already be above 50%. Variable income makes things harder too. If your paycheck changes each month, the rule still works, but you’ll need to budget from a lower baseline or use average income.

The rule is a guide, not a law. If your numbers don’t fit, that’s useful information, not failure.

Some critics also argue that 30% for wants feels high if you’re behind on savings or trying to wipe out debt fast. Others say 20% isn’t enough if you’re starting late on retirement. Those are fair concerns, which is why many people adjust the rule instead of following it exactly. A good rundown of the pros and cons of the rule can help you decide if it matches your season of life.

How to make the 50/30/20 rule work in real life

The best budget is the one you’ll use next month, not the one that looks perfect on paper.

Common mistakes that can throw off your budget

The first mistake is using gross income. That one error can wreck the whole plan before it starts.

The second is guessing. People often think they spend $400 on food, then find out it’s closer to $700 once takeout, snacks, and delivery fees show up. Track your spending before you judge the rule.

Another common problem is mixing up categories. A gym membership may feel like a need, but for most people it’s a want. Minimum credit card payments belong in needs, while extra credit card payments belong in savings or debt payoff.

Finally, don’t treat big future goals like random extras. Car repairs, holiday spending, and a future move should usually be planned in the 20% bucket, not brushed off as wants.

What to do if your needs are already more than 50%

Start with the easiest lever: trim wants for a season. That may free up cash fast.

Next, look at fixed costs. Rent, car payments, insurance, and phone plans usually matter more than cutting one streaming service. Even a small drop in monthly fixed bills can change the whole picture.

You can also raise income. Overtime, freelance work, a second job, or a higher-paying role may help if your essentials are already stretched thin.

If nothing moves right away, use a modified split. For example, 60/20/20 may fit better during a high-rent season. Some people prefer 50/20/30 when they want to put more money toward savings or debt. In 2026, with costs still elevated, some households even use 70/20/10 for a while. The goal is progress, not purity.

Simple tips to stay on track each month

Track your spending for one to two months first. That gives you real numbers, not guesses.

Then automate what you can. Move savings on payday so it doesn’t sit in checking and disappear.

Also, review your budget once a month. Prices change, bills shift, and life rarely stays still. A budget should move with you.

If you want less manual work, use your bank app or a budgeting tool to sort spending into broad buckets. That’s often enough to spot patterns and make better decisions.

Budgeting feels hard when every dollar seems to float around with no job. The 50/30/20 rule gives those dollars simple roles: cover needs, enjoy some wants, and build the future.

Use it as a starting point, not a scorecard. If your real life calls for a different split, adjust it and keep going.

Take five minutes today, calculate your three numbers from take-home pay, and use them as your first budget draft. That small step can turn money stress into a plan.